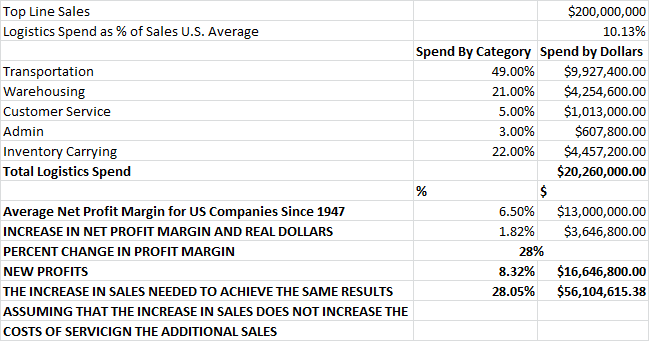

Risk Pooling is very much like the idea of Portfolio Management in the Financial Industry where Risks i.e. costs are hedged by properly managing the portfolio of the Insurance or Mutual fund in order to balance risks and gain long term Portfolio performance.

In this example we will look at to DCs using the formula:

Using these two formulas together, we are basically looking for an optimal decision on whether to centralize the inventory for a given SKU based on whether the correlation in demand will yield a lower Safety Stock, and obviously when SS is Inventory levels for the Product is lowered through out the entire Supply Chain. In a properly managed Supply Chain which is optimized for Cost and Customer service, SS is the barometer by which a SKU can quickly be judged. If SS is high, then variance and customer service requirements are also likely to be high, when SS is low then we know that variance is typically reasonably low as well.

In this example we will look at to DCs using the formula:

where

| SS1 | Safety stock in location 1 | ||||||

| SS2 | Safety stock in location 2 | ||||||

| SSc | Safety stock in centralized location | ||||||

| s1 | Std. deviation of lead time demand in location 1 | ||||||

| s2 | Std. deviation of lead time demand in location 2 | ||||||

| sc | Std. deviation of lead time demand in centralized location | ||||||

| p12 | Correlation of demand in locations 1 and 2 | ||||||

| Example | ||||||||

| sigma | 1. Safety stock in location 1? | |||||||

| Location 1 | 45 | 2. Safety stock in location 2? | ||||||

| Location 2 | 55 | 3. Combined safety stock (2 locations)? | ||||||

| 4. Pooled std. deviation of lead time demand? | ||||||||

| p12 | 0.9 | 5. Pooled safety stock? | ||||||

| alpha | 97% | 6. Portfolio effect (SS reduction)? | ||||||

| z | 1.88 | |||||||

Using these two formulas together, we are basically looking for an optimal decision on whether to centralize the inventory for a given SKU based on whether the correlation in demand will yield a lower Safety Stock, and obviously when SS is Inventory levels for the Product is lowered through out the entire Supply Chain. In a properly managed Supply Chain which is optimized for Cost and Customer service, SS is the barometer by which a SKU can quickly be judged. If SS is high, then variance and customer service requirements are also likely to be high, when SS is low then we know that variance is typically reasonably low as well.

I think this next chart will help to conceptualize the idea behind using Risk Pooling:

As you can see in this chart, SKU ABC from both Loc1 and Loc2 are close to having a -1 correlation. When demand for the SKU from Loc 1 is high, the demand from Loc2 is low, by combining this SKU into 1 well place Distribution Center the average demand becomes very predictable meaning that Inventories and SS can also be lowered. When analyzing across many SKUs you can quickly see how Inventory Carrying Costs can be greatly lowered. Of course you will need to factor other SC costs to see if there is a NET benefit, but it has been my experience that after doing a deeper dive into consumer data that you will quickly see that there is a huge Net Benefit, and that you can use an existing warehouse by simply changing some Supply Chain policies.

I hope that I covered this topic well, please feel free to email me with any questions.